What Is the EU ETS?

The EU ETS, European Union Emissions Trading System, is the European system for trading emission allowances. It is one of the main tools used by the European Union to regulate greenhouse gas emissions from the most emissions-intensive industrial sectors, by introducing a price for every tonne of CO₂ equivalent emitted.

The system is based on a simple principle: emissions have a cost, and this cost must be integrated into business decisions. For the companies involved, the EU ETS is therefore not only an environmental regulation, but also an economic mechanism that affects operating costs, industrial investments, energy management, procurement, and competitiveness.

The EU ETS works according to a cap-and-trade model. The European Union sets a maximum limit on the total emissions of the sectors covered by the system. Within this limit, companies must hold enough emission allowances to cover their annual emissions. One allowance, called an EUA, European Union Allowance, permits the emission of one tonne of CO₂ equivalent. The cap is reduced over time, making allowances progressively scarcer and increasing the economic incentive to reduce emissions.

For a company, this means that emissions are no longer just a metric to monitor, but an economic variable to manage. Reducing emissions can reduce exposure to the cost of allowances. Failing to do so can increase the risk of rising costs and lower competitiveness in markets where climate performance is becoming increasingly relevant.

To learn more about measuring emissions at company level, you can also read the guide to carbon footprint.

How the cap-and-trade system works

Under the EU ETS, every year companies subject to the mechanism must monitor their emissions, have them verified by an accredited body, and surrender a number of allowances equivalent to the emissions produced.

Allowances can be purchased through auctions, received for free in certain cases, or traded on the market. The system therefore creates a CO₂ market: companies that reduce emissions may need fewer allowances, while those that continue to emit must bear a higher cost to cover their emissions.

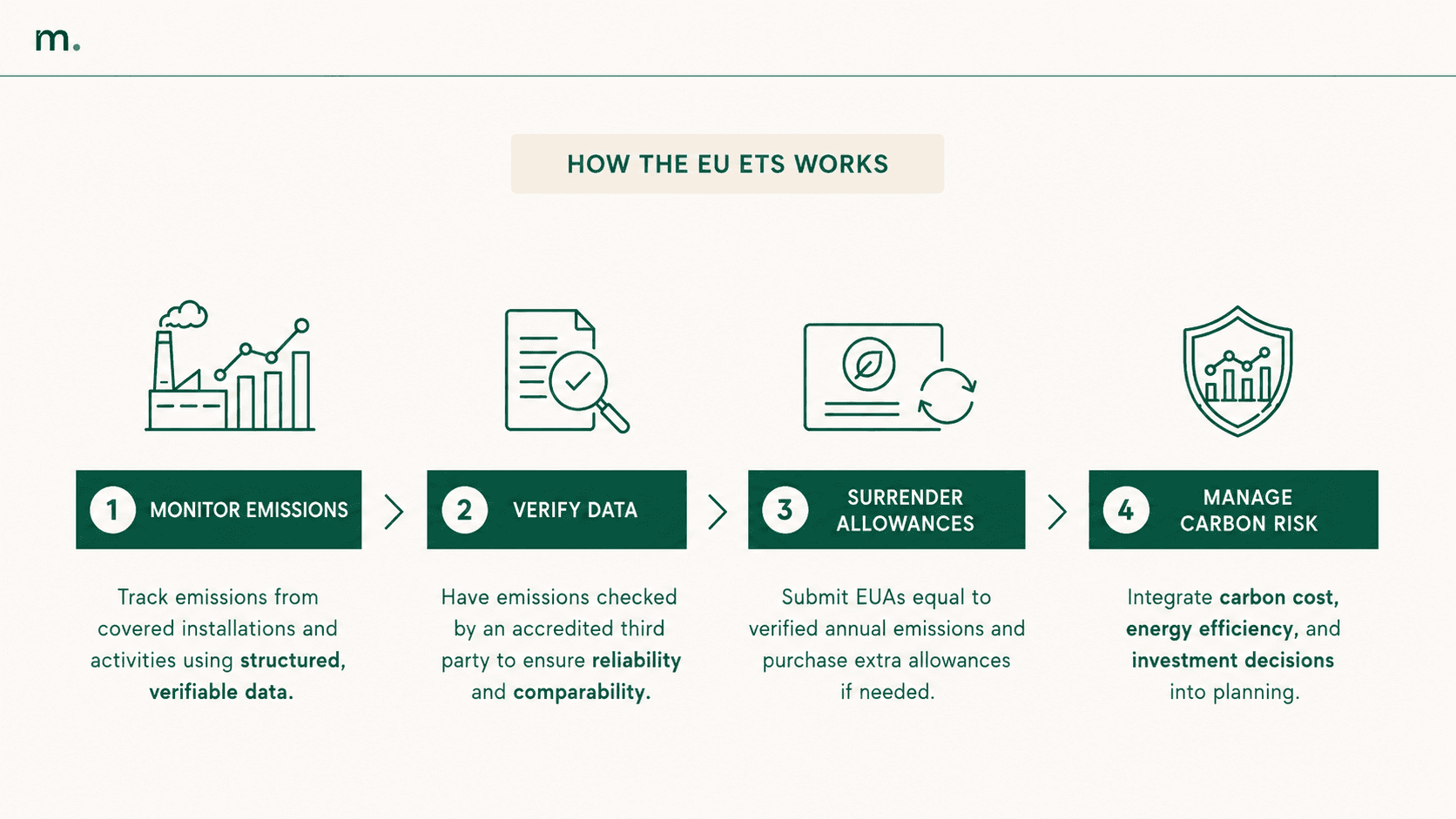

The operational process can be understood in four steps.

The first is monitoring. The company measures the emissions produced by the installations or activities covered by the system, according to defined and documentable methodologies. In this process, emissions calculation software can provide support.

The second is verification. The data must be checked by accredited third parties, because the system relies on information that is reliable and comparable.

The third is the surrendering of allowances. The company must surrender a number of allowances equal to its verified emissions. If it has emitted more than expected, it will need to purchase additional allowances. If it has reduced its emissions, it can reduce its allowance requirements.

The fourth is the strategic management of carbon risk. Companies need to assess how allowance price trends, energy efficiency, technology investments, and production choices affect future costs.

This is the most important point for companies: the EU ETS is not only about annual compliance, but about the ability to anticipate the economic impact of emissions over the medium term.

Which companies fall under the EU ETS?

The EU ETS mainly applies to high-emission sectors. These include electricity and heat generation, refineries, steel, cement, glass, paper, ceramics, chemicals, fertilizers, and other regulated industrial sectors.

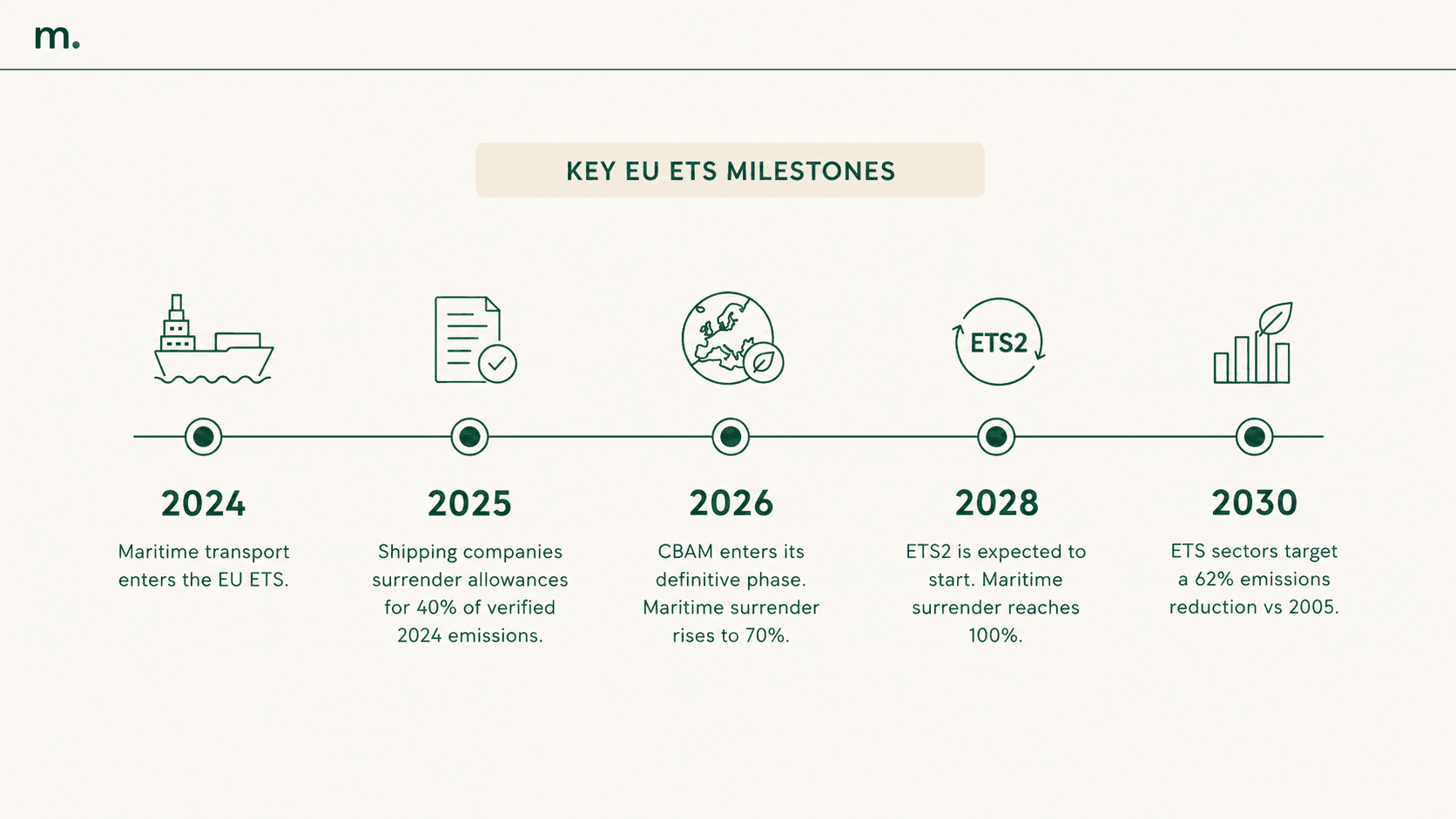

Over time, the scope of the system has expanded. In addition to industrial and energy installations, the EU ETS also includes aviation for specific routes and, since 2024, maritime transport. The extension to maritime transport applies in particular to large ships above 5,000 gross tonnage, with a progressive application of allowance surrender obligations.

Companies that are not directly included in the system can also be affected by the EU ETS. This happens when they purchase materials, energy, components, or services from suppliers subject to the system. In these cases, the cost of carbon can be reflected in purchase prices, supply conditions, and requests for environmental data along the supply chain.

For this reason, the EU ETS is relevant not only for companies formally covered by the regulatory perimeter, but also for industrial companies that need to manage energy costs, indirect emissions, customer requests, and supply chain-related risks.

The latest updates on the EU ETS

In recent years, the EU ETS has been strengthened through the European Fit for 55 climate package. The objective is to align the system with the European Union’s emissions reduction trajectory for 2030.

One of the main updates concerns the new reduction target for the sectors covered by the EU ETS. The system has been revised to bring ETS emissions down by 62% by 2030 compared to 2005 levels. To achieve this target, the linear reduction factor of the cap has been increased to 4.3% per year for the 2024–2027 period and to 4.4% per year from 2028.

A second update concerns the inclusion of maritime transport. Since 2024, emissions from the maritime sector have progressively entered the system. Shipping companies must surrender allowances for 40% of verified 2024 emissions in 2025, 70% of 2025 emissions in 2026, and 100% of emissions from 2027 onwards.

A third element concerns the connection with CBAM, the Carbon Border Adjustment Mechanism. CBAM will enter its definitive phase from 2026, after the 2023–2025 transitional phase, and has been designed to progress alongside the gradual phase-out of free allowances in the covered sectors. The objective is to prevent production from being relocated to countries with less stringent climate rules, while maintaining more balanced conditions between European producers and importers.

Finally, ETS2 is expected to launch as a system separate from the current EU ETS, dedicated to emissions from fuel combustion in buildings, road transport, and additional sectors, mainly small industry not covered by the existing ETS. ETS2 is expected from 2027 and will be an important element in extending carbon pricing to sectors that have so far been regulated through different tools.

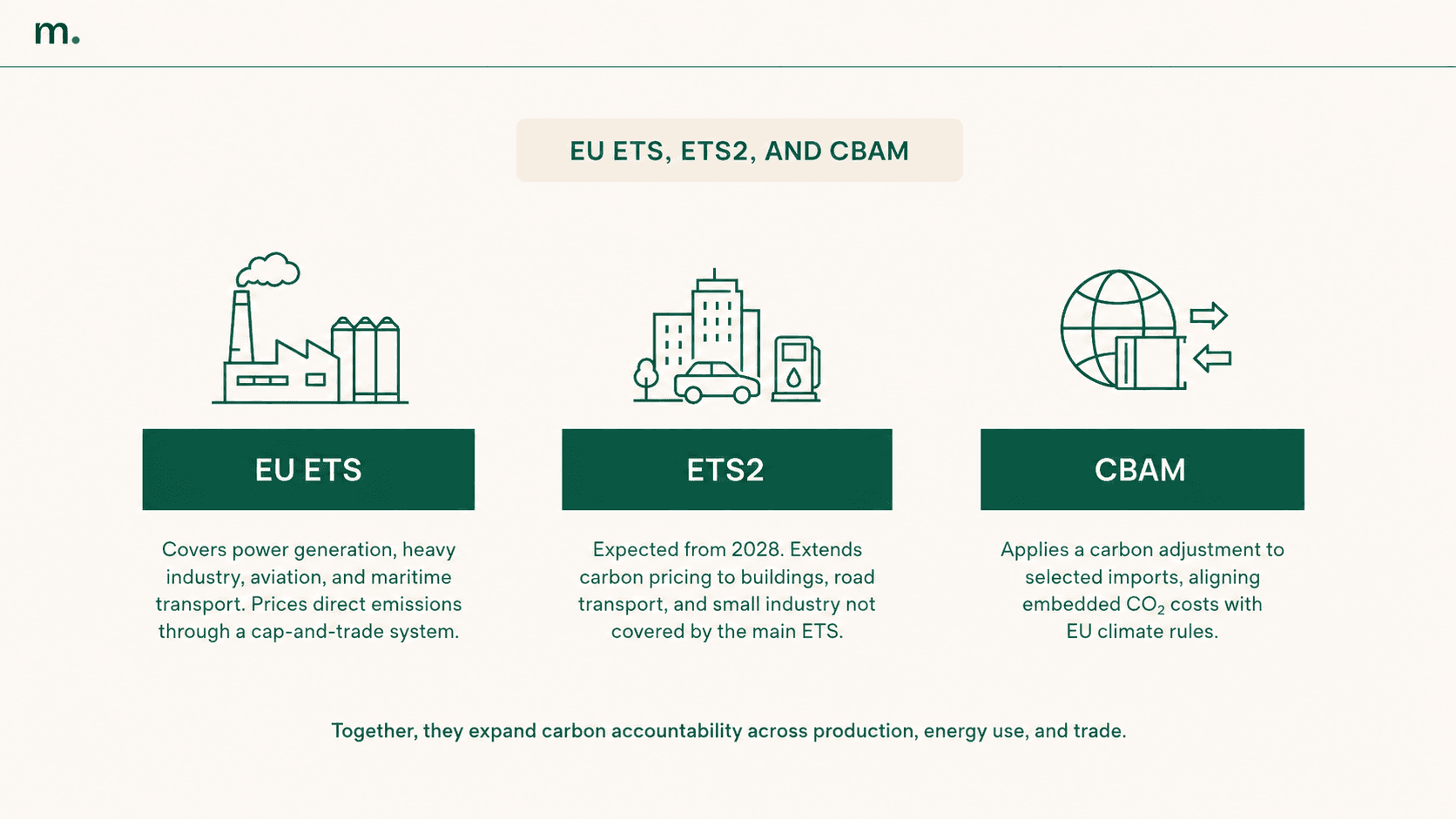

EU ETS, ETS2, and CBAM: what is the connection?

EU ETS, ETS2, and CBAM are different instruments, but they follow the same regulatory direction: transforming emissions into a measurable and manageable economic factor.

The EU ETS covers large industrial installations, energy, aviation, and maritime transport. ETS2 will extend a similar logic to fuels used in buildings, road transport, and other sectors not covered by the main system. CBAM, on the other hand, applies a carbon adjustment mechanism to imports of certain goods, with the aim of aligning the cost of CO₂ embedded in imported products with the cost borne by European producers.

The connection between ETS and CBAM is particularly important because the definitive introduction of CBAM is taking place in parallel with the gradual phase-out of free ETS allowances. For companies importing goods covered by the regulation, this means managing emissions data, declarations, and compliance requirements with greater precision. To explore the mechanism in more detail, you can read the dedicated guide to CBAM.

“ETS2 and CBAM should not be seen as isolated tools, but as part of a broader industrial trajectory. Carbon pricing can become a competitiveness lever for Europe only if it is supported by investments in infrastructure, production capacity, clean energy, and strategic supply chains. The challenge is not only to make the cost of emissions more visible, but to turn it into a concrete strategy for industrial modernization and energy autonomy.”

— Alessandro Nora, CEO and co-founder of Metrikflow

From an operational perspective, the central issue is data quality. Companies need to collect information on the emissions embedded in imported goods, verify its consistency, and keep it updated over time. In this context, CBAM software can help structure data, declarations, and compliance obligations in a more traceable way.

What changes for companies?

For companies subject to the EU ETS, the first impact is compliance. Monitoring, reporting, verification, and the surrendering of allowances must be managed through rigorous processes, reliable data, and clear responsibilities.

The second impact is economic. The price of allowances can affect industrial costs and financial planning. A company that does not integrate the cost of carbon into its decisions risks underestimating the real cost of processes, products, and investments.

The third impact concerns industrial strategy. As the cap decreases and allowances become scarcer, reducing emissions becomes a lever to protect margins, competitiveness, and business continuity. Energy efficiency, electrification, renewable energy, process changes, and technological innovation are no longer just environmental initiatives, but industrial decisions with measurable economic effects.

The fourth impact concerns the supply chain. Companies that are not directly subject to the ETS can still experience indirect effects through higher costs for energy, materials, and components purchased from regulated suppliers. In this case, it becomes important to understand how direct and indirect emissions are distributed across business activities, purchased energy, and the value chain. To explore this distinction, it can be useful to start from the guide to Scope 1, 2, and 3 emissions.

The fifth impact concerns data quality. The EU ETS requires solid, verifiable information connected to real processes. This approach is becoming increasingly relevant even outside the ETS perimeter, because customers, investors, and industrial value chains are asking for more granular data on the carbon footprint of products, activities, and supplies.

How to prepare for the EU ETS operationally

To manage the EU ETS effectively, companies need to avoid a purely reactive approach. Waiting for the annual deadline to collect data, calculate emissions, and manage allowances increases the risk of errors, inefficiencies, and delayed decisions.

The first step is to build a solid data foundation. Direct emissions, energy consumption, fuels, emission factors, production data, and process information must be collected in a structured and verifiable way.

The second step is to connect emissions data to operational processes. The goal is not only to know how many tonnes of CO₂ equivalent have been emitted, but to understand which installations, lines, materials, or processes generate the highest exposure.

The third step is to integrate the cost of carbon into business decisions. This means evaluating scenarios: what happens if allowance prices increase? What is the economic return of an investment in energy efficiency? Which processes expose the company to greater carbon risk? Which suppliers can reduce indirect impact?

The fourth step is to connect compliance with the reduction plan. The EU ETS should not be managed as a separate obligation, but as part of a broader strategy for decarbonization, cost control, and industrial performance. To explore this aspect further, you can also read the article on strategies to reduce Scope 1, 2, and 3 emissions.

Conclusion

The EU ETS is much more than an emissions allowance market. It is a mechanism that transforms CO₂ into an economic and strategic variable for companies.

For directly covered companies, it means managing obligations related to monitoring, verification, and the surrendering of allowances. For companies that are not directly included, it means understanding how the cost of carbon can affect energy, materials, suppliers, products, and competitiveness.

Recent updates make the system even more relevant: a faster reduction of the cap, the inclusion of maritime transport, the gradual phase-out of free allowances, the connection with CBAM, and the introduction of ETS2. For companies, this requires a more structured approach to managing emissions data and carbon-related risks.

The priority is not only to comply with the regulation. It is to build processes capable of turning emissions management into a lever for efficiency, cost control, and industrial planning.

CONTRIBUTOR

Alessandro Nora

CEO & Co-founder

Alessandro's goal is to make a real impact on sustainability. After founding a sustainable fashion marketplace, he decided to focus on ESG digitalisation with the aim of making sustainability more concrete, measurable and accessible for companies. A careful and methodical founder, with experience in Genoa, Berlin and Lisbon, Alessandro combines international vision and operational rigour in the development of digital solutions that simplify ESG regulations and compliance, supporting companies in adapting to ESG regulations, certifications and ratings through structured and audit-ready tools. Topics covered: CSRD, CSDDD, EUDR, CBAM ESG ratings, ESG certifications, Ecovadis, sustainability governance, regulatory compliance.

Stay up to date with Metrikflow Insights!

We deliver expert insights, product updates, industry trends, and actionable strategies straight to your inbox. Stay ahead in ESG, GHG, and LCA — one edition at a time.

By submitting this form, you consent to receive the requested resource. For more information on how we process and protect your data, view our Privacy Policy.